Ecobank

Barriers: Creating a Fast, Reliable, and Accessible Ecobank App

Problem Statement

Context

Ecobank operates across 33 African countries, serving millions of customers in diverse economic and technological environments. A significant portion of the user base relies on entry-level smartphones with limited processing power, storage capacity, and RAM, while operating on 2G/3G networks with inconsistent connectivity and high data costs. This digital divide creates barriers to financial inclusion, as traditional banking apps often fail to function effectively on these constrained devices.

Current market research indicates that over 60% of smartphone users in Ecobank's key markets use devices with less than 2GB RAM and frequently experience network speeds below 1Mbps. These users represent a crucial demographic for financial inclusion initiatives, but are underserved by conventional mobile banking solutions that prioritize feature richness over accessibility.

Challenge

How might we design a lightweight version of the Ecobank mobile application that performs reliably on low-end devices and slow internet connections, while still providing users with secure, seamless access to essential banking services?

Key Challenge Areas:

Technical Performance: Ensuring app responsiveness on devices with limited processing power and memory

Connectivity Resilience: Maintaining functionality during network interruptions and slow data speeds

Data Efficiency: Minimizing data consumption to reduce costs for price-sensitive users

Security Balance: Implementing robust security without compromising performance

Feature Prioritization: Determining which banking services are truly essential versus nice-to-have

User Experience Consistency: Maintaining intuitive navigation despite simplified interface requirements

Objectives

Accessibility: Enable 95% of users with entry-level devices to achieve core banking transactions successfully

Performance: Achieve app launch times under 3 seconds and transaction completion under 10 seconds on target devices

Data Efficiency: Reduce data consumption by 70% compared to the full application while maintaining functionality

Offline Capability: Provide essential account information and transaction history access during connectivity gaps

User Adoption: Achieve 40% adoption rate among target user segment within 12 months

Customer Satisfaction: Maintain NPS score above 60 despite simplified feature set

Security Compliance: Meet all regulatory requirements while optimizing for performance

Scalability: Design architecture to support rapid user growth across multiple markets

Role

Design a comprehensive UX strategy for Ecobank's lightweight mobile application, combining user research across African markets with accessibility design principles. By combining user research, content strategy, and UX design, I worked to create optimized digital banking touchpoints that served essential financial needs for underbanked users while achieving Ecobank's financial inclusion and market expansion goals.

Success Criteria

How to measure this project's success

Data Efficiency

User Trust & Transparency

User Satisfaction

Performance & Speed

Accessibility & Compatibility

Core Feature Coverage

App loads under 5s on 3G connections.

Key actions (login, balance check, transfer) complete in under 10 seconds.

Runs smoothly on low-end Android devices (2GB RAM or less).

Offline-first support: basic features (e.g., viewing recent transactions)

Complete essential tasks: account overview, fund transfers, bill...etc

Advanced features (e.g., investment services, detailed analytics) available in the full version.

App consumes minimal data (<1MB per session for common tasks).

Lightweight updates (smaller package size compared to full app).

Real-time feedback even with weak connectivity.

Consistent security (PIN, OTP, biometrics fallback) without adding performance overhead.

Target improvement in app store ratings (4★ and above) from users citing performance and accessibility.

Reduced complaints about crashes, slowness, or device incompatibility.

Outcomes

By following this roadmap, Ecobank can deliver a fast, reliable, data-efficient banking experience to millions of users in West Africa who currently struggle with performance and accessibility issues.

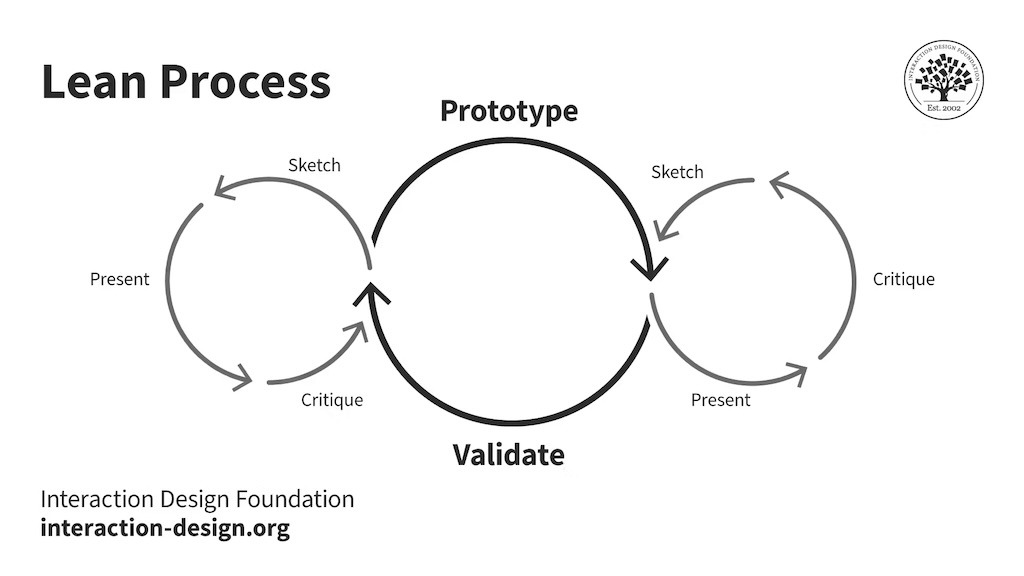

Lean Design framework

The Lean UX process focuses the design team on the user experience in an effort to cut waste while saving money and resources.

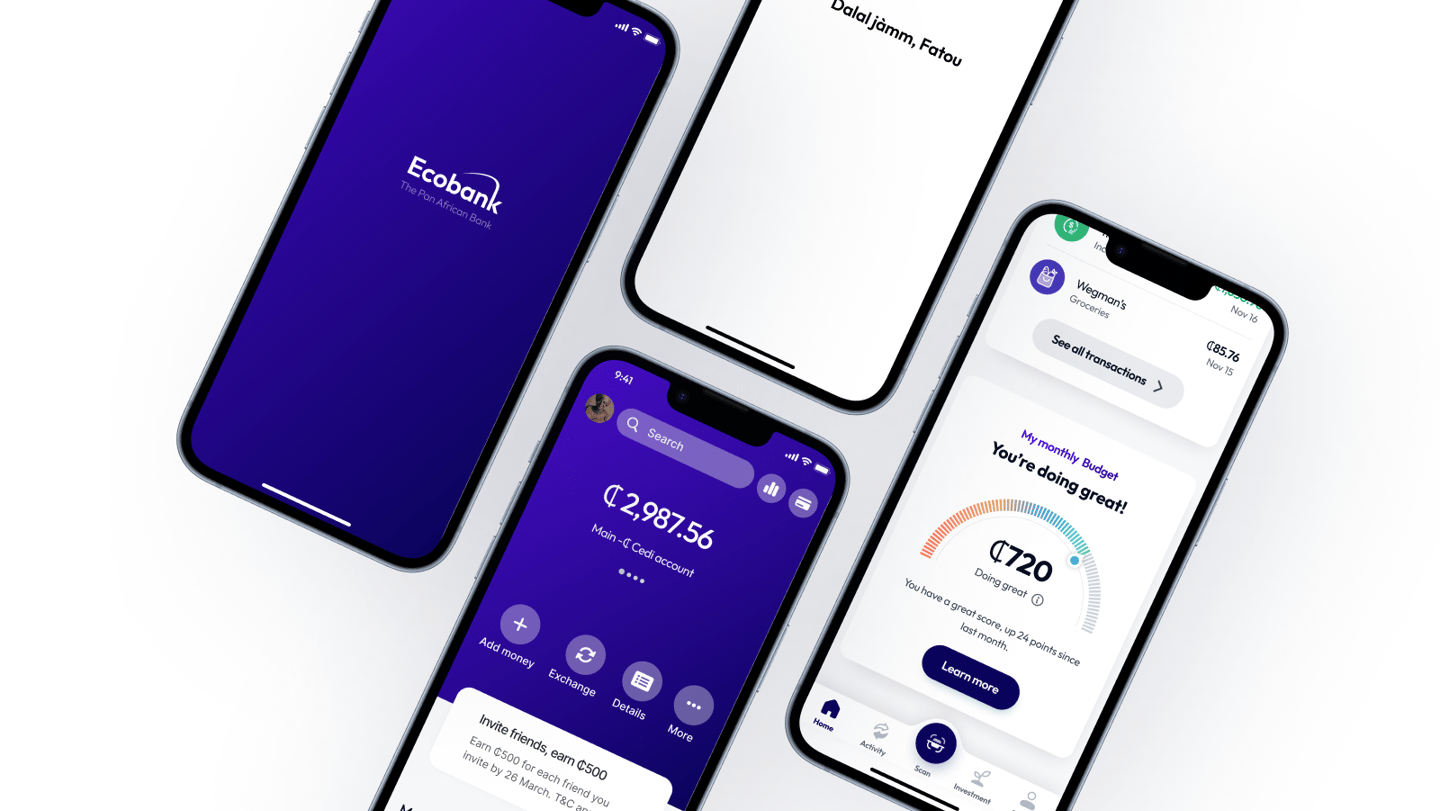

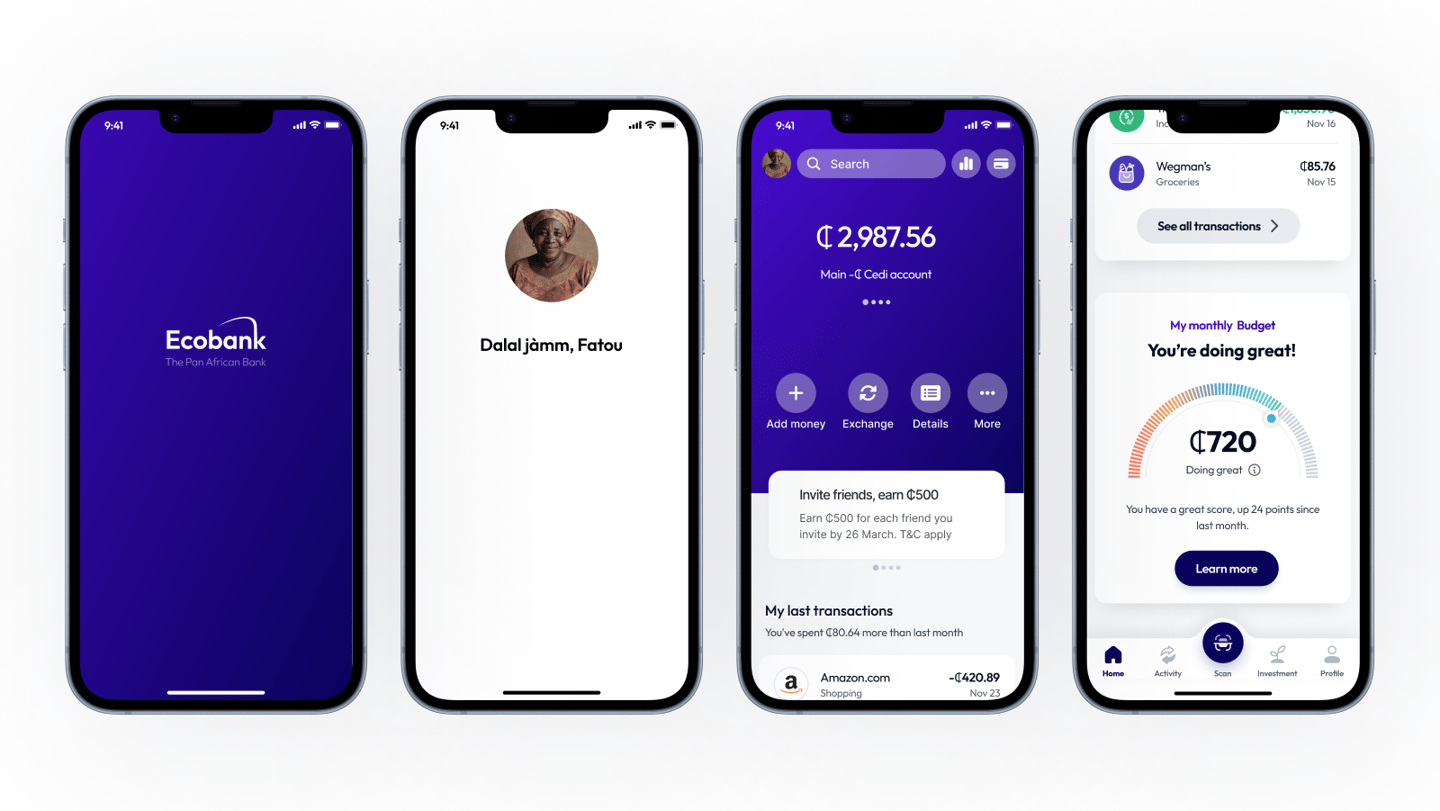

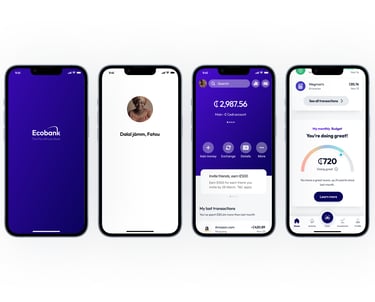

MAKE

Translate insights into concepts, prototypes, and minimum viable solutions. Focus on speed, iteration, and building just enough to test

CHECK

est designs with real users to validate assumptions.

Gather feedback, measure outcomes, and refine the solution.

THINK

Research users, map their pain points, and frame the design challenge. Define clear opportunities before moving into solution mode.

Think

1. Research

Objective: Understand user pain points, constraints, and context in West Africa.

User Context (West Africa)

Smartphone penetration: In Sub-Saharan Africa, 70% of connections are smartphones, but ~48% are low-end Androids with ≤2GB RAM (GSMA Mobile Economy Report, 2024).

Network quality: About 45% of users in West Africa rely on 3G and only 15% on 4G/5G (GSMA, 2023).

Data costs: 1GB of mobile data costs 3–5% of monthly income in Nigeria and Ghana, making data-heavy apps a barrier (Alliance for Affordable Internet, 2024).

User Feedback (Ecobank app)

Play Store rating: 3.1/5 (Nigeria, 2025).

Top complaints: app crashes, slow load times, failed transactions without refunds, heavy on storage/data.

Key Insight: Users want reliable, lightweight access to essential banking features (check balance, transfer money, pay bills) without heavy data or device requirements.

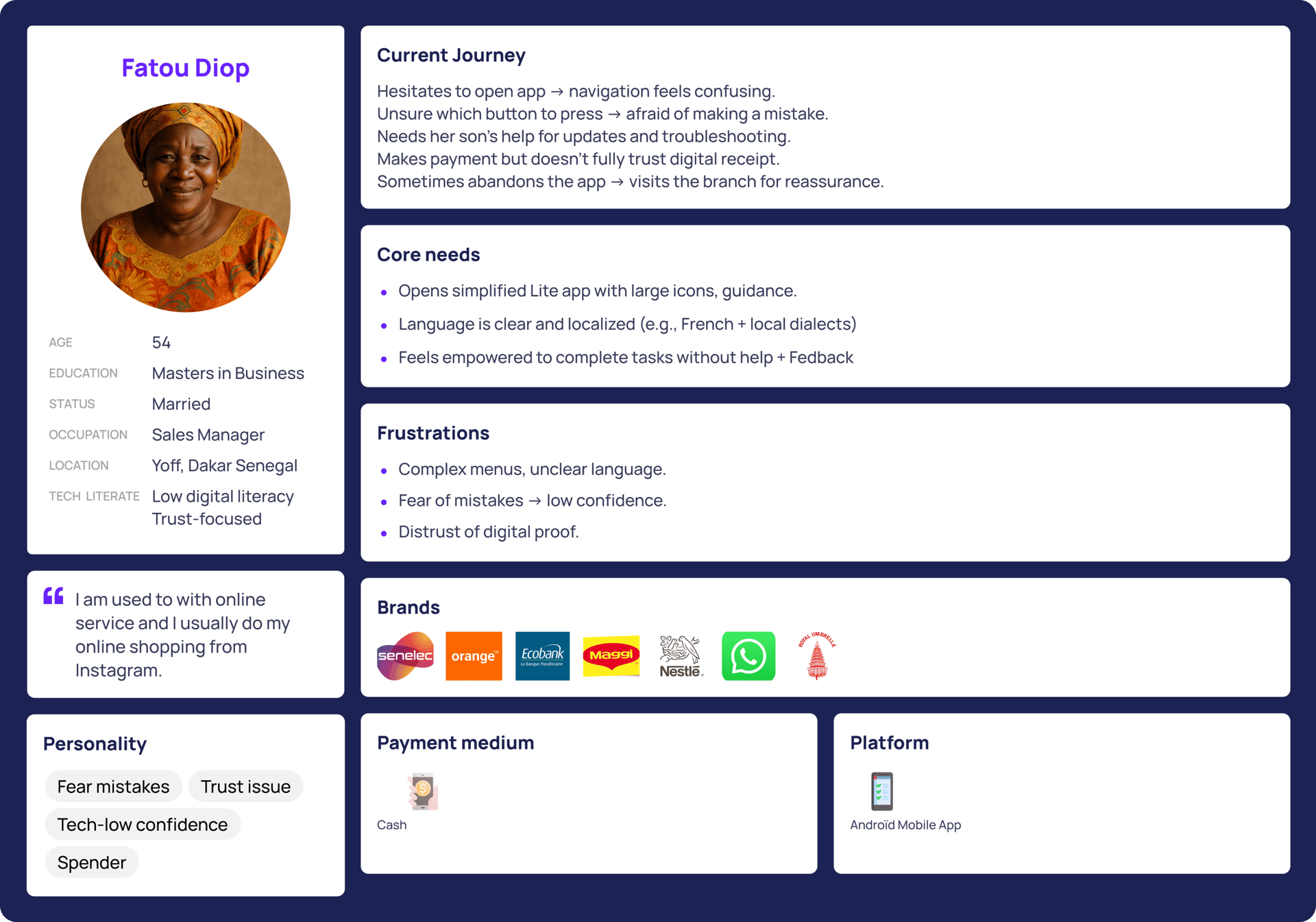

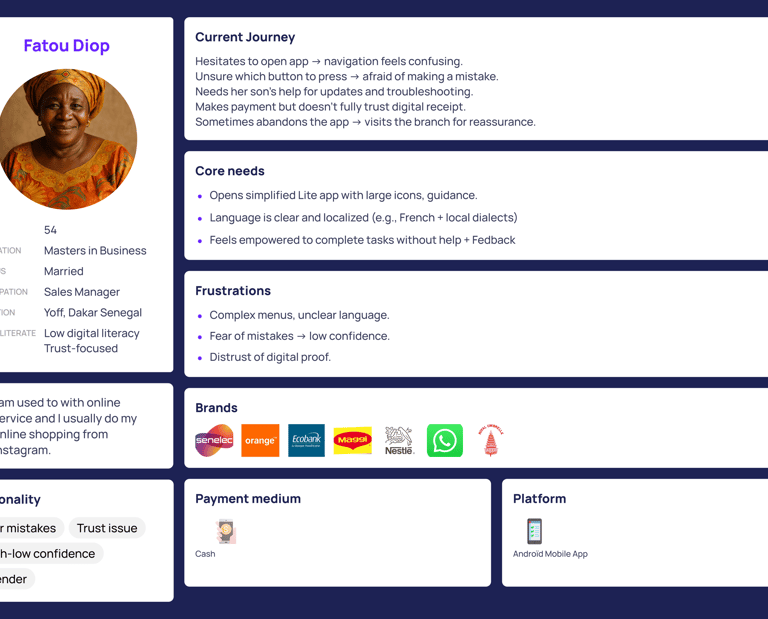

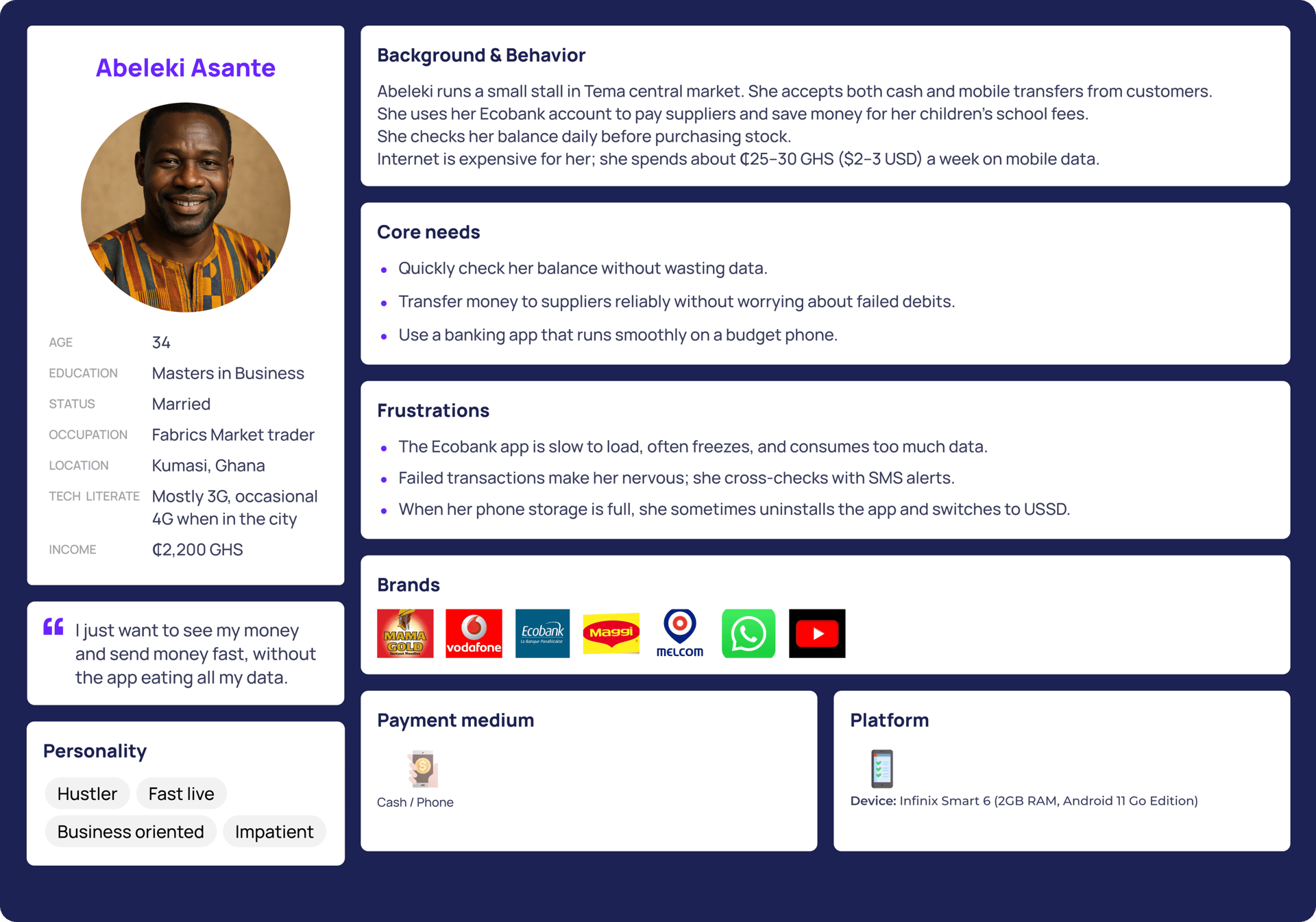

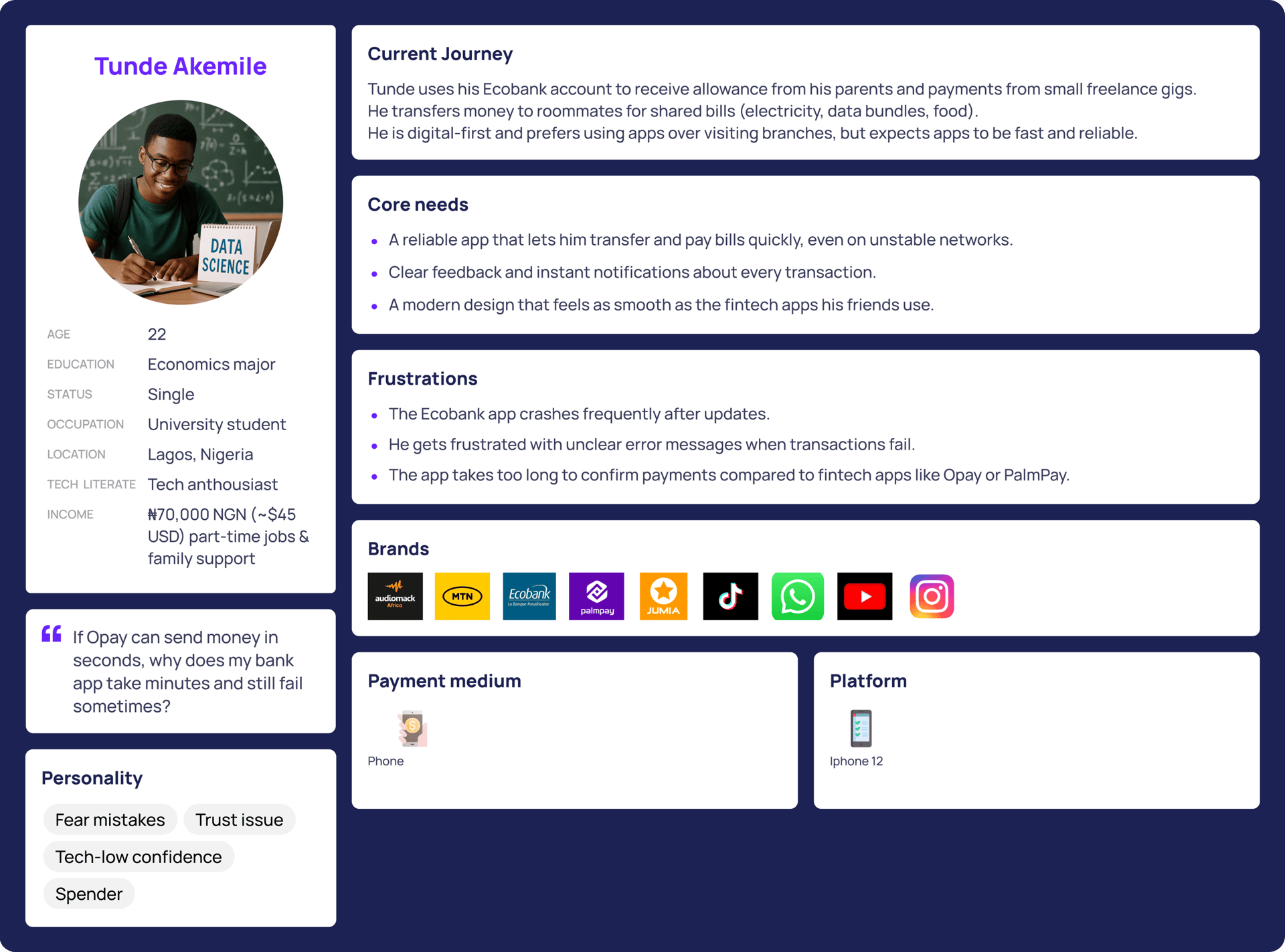

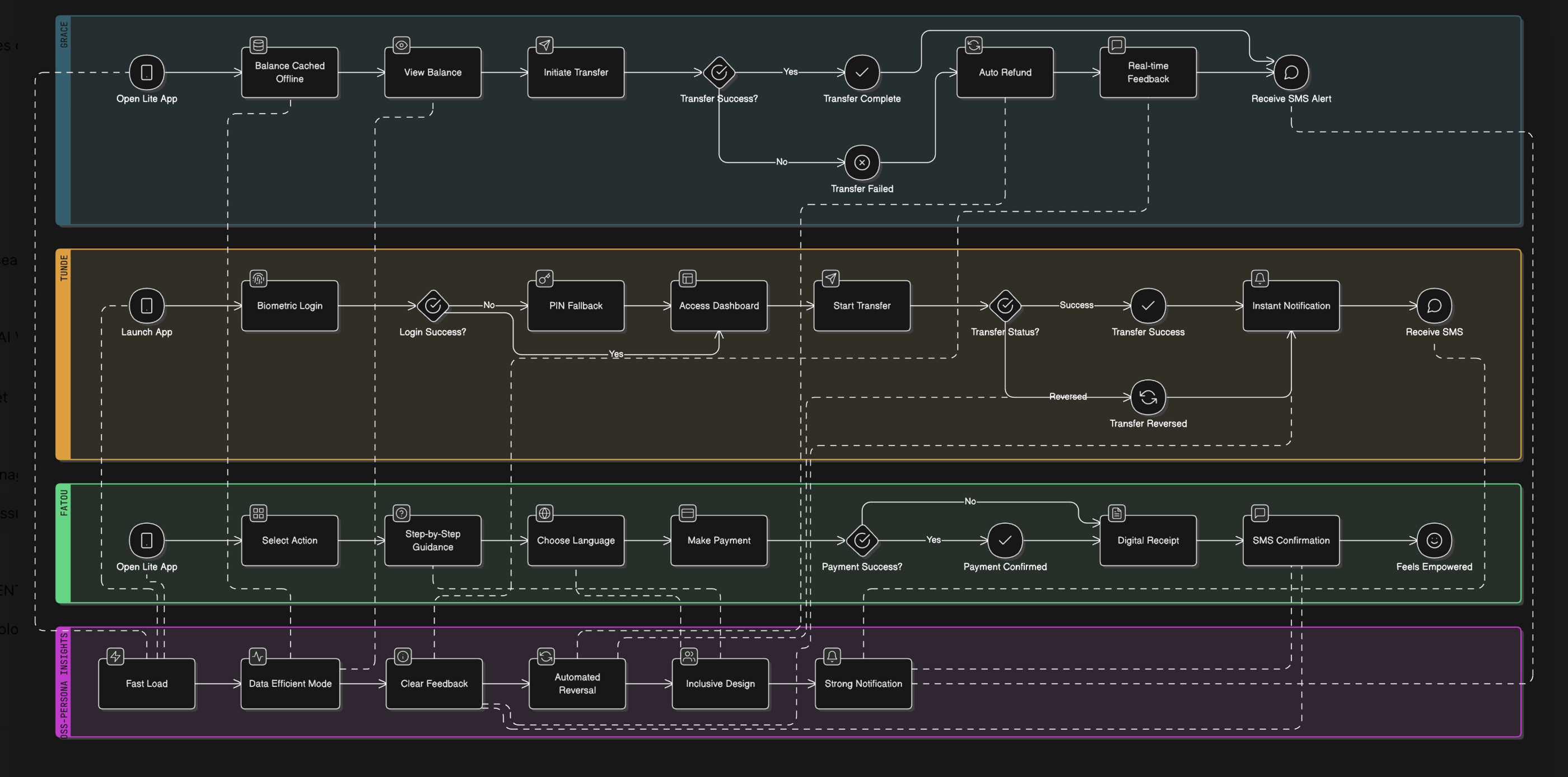

Users Personae

Working with two user personas that are grounded in real insights about West African mobile banking users. These personas will reflect the performance & accessibility challenges to which I'll be Adding a third persona—a 54-year-old family mother, less comfortable with digital tools—broadens the perspective. It captures a segment often overlooked in digital banking: older users who are financially active but hesitant about technology.

Cross-Persona Insights

Common Pain Points: Slowness, unclear feedback, and reliability gaps.

Opportunities Across All Personas:

Lite performance (fast load, low data, smooth on low-end phones).

Clear feedback (transaction status, refunds, notifications).

Inclusive design (simplified flows for less tech-savvy users).

Users Journey mapping

2. Ideation

Opportunity Areas:

Lite Experience → Focus only on essential features.

Offline-first banking → Allow users to view balances & recent transactions offline, sync later.

Data-efficient design → Compress images, minimize animations, allow low-bandwidth mode.

Progressive disclosure → Start with core services; load advanced features on demand.

4. Behavior Models

Habitual Use: Users check balances several times per week (often before transfers).

Backup Behaviors: If the app fails, many switch to USSD banking or cash.

Device Switching: High device turnover due to affordability → users need easy migration between devices.

Trust Gaps: Users often cross-check app results with SMS alerts for confirmation.

3. Mental Models

How users think about banking tasks in West Africa:

“Check my balance first.” → Assurance that money is safe.

“Send money quickly.” → Transfers to family, school fees, bills are time-sensitive.

“Data is precious.” → Minimize usage.

“If it fails, I lose money.” → Fear of failed transactions drives preference for physical branches or USSD codes.

Implication: The app should align with these models → fast balance check, trustworthy transaction flows, transparent feedback, and minimal data use.

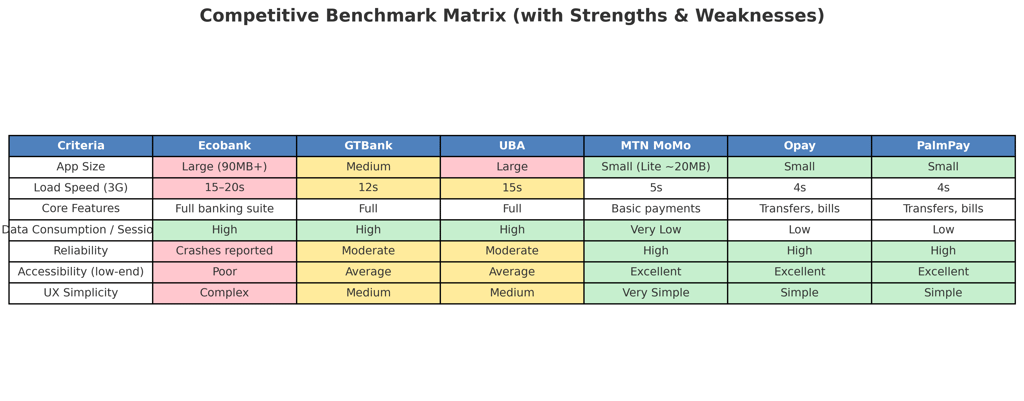

6. Competitive Analysis

Direct & Indirect Competitors in Africa:

GTBank (Nigeria): Offers both app + strong USSD fallback, highly adopted in rural areas.

UBA Leo App (Nigeria): AI-powered chatbot banking but criticized for being data-heavy.

MTN MoMo (Ghana, Nigeria, Côte d’Ivoire): Simple, lightweight, and offline-first; strong adoption in low-income segments.

Opay (Nigeria): Known for fast transactions, low data use, and targeting small-device users.

Key Differentiator for Ecobank: A hybrid approach → secure bank-grade app, but designed with the efficiency of a fintech lite app (fast, data-light, accessible on low-end devices).

5. Hypothetical Test Results

Based on secondary research + comparable fintech apps in West Africa)

A Nigerian fintech case study (Flutterwave, 2023) showed drop-off rates increased 60% when load times exceeded 5 seconds.

MTN Mobile Money research (Ghana, 2022) found that lite versions increased daily active usage by 25% in low-connectivity areas.

In Ecobank user reviews (Google Play Nigeria, 2024), 40% of 1-star reviews mention “slow,” “crash,” or “failed transaction.”

Implication: Performance fixes + lightweight design could increase adoption by 20–30% among underserved users.

Summary of THINK Phase:

The evidence is clear: Ecobank users in West Africa face device, connectivity, and trust barriers. A lightweight app focused on speed, accessibility, and reliability can bridge this gap and position Ecobank as both a modern and inclusive digital bank.

Make